Trends in Chinese International Education 2026: Key Takeaways from WIEC April 2026

Last week, Sunrise International presented at the Washington International Education Conference (WIEC), sharing the latest market intelligence on Chinese student recruitment with university leaders and higher education professionals across the United States. Below are the key findings from our 2026 trends analysis.

Two Simultaneous Truths

2025 was arguably the most disruptive year for US–China student recruitment since COVID. Yet the headline numbers tell two very different stories — and understanding both is essential for institutions making recruitment decisions in 2026.

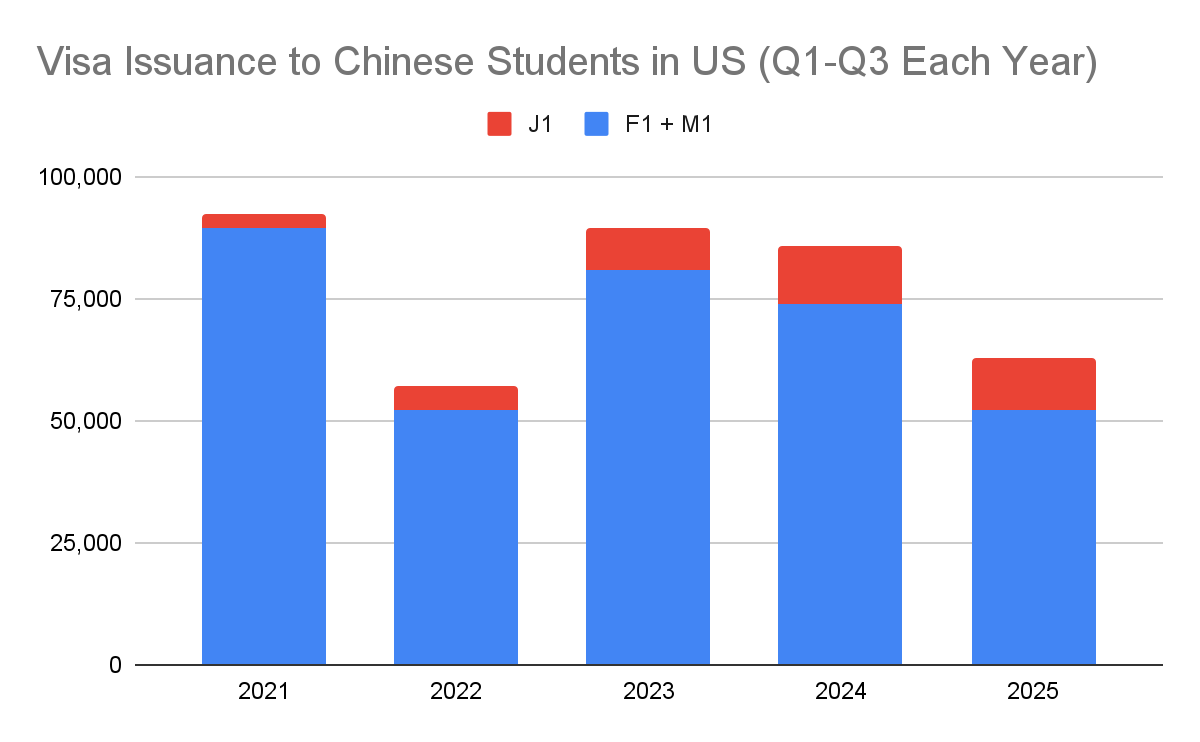

On one hand, US F-1 visa issuance to Chinese students fell approximately 29% in Q1–Q3 2025. A May–June policy freeze caused a 50% single-month collapse across all visa categories, and the year was marked by policy whiplash: aggressive revocation announcements walked back within weeks, proposed enrollment caps, and ongoing legal battles over SEVP certifications.

On the other hand, Chinese students showed far greater resilience than any other major sending country. India saw a 62% decline. Nepal fell 72%. Nigeria dropped 52%. China's decline was less than half of India's — and upstream demand indicators remained stable throughout: Common App applications from China were essentially flat year over year, Harvard's Chinese cohort grew 4.5%, and the number of study-abroad agency firms in China surged 252% since 2021.

The question isn't whether demand from China is declining. It isn't. The question is which number is the signal — and which is the noise.

Where Chinese Students Are Going

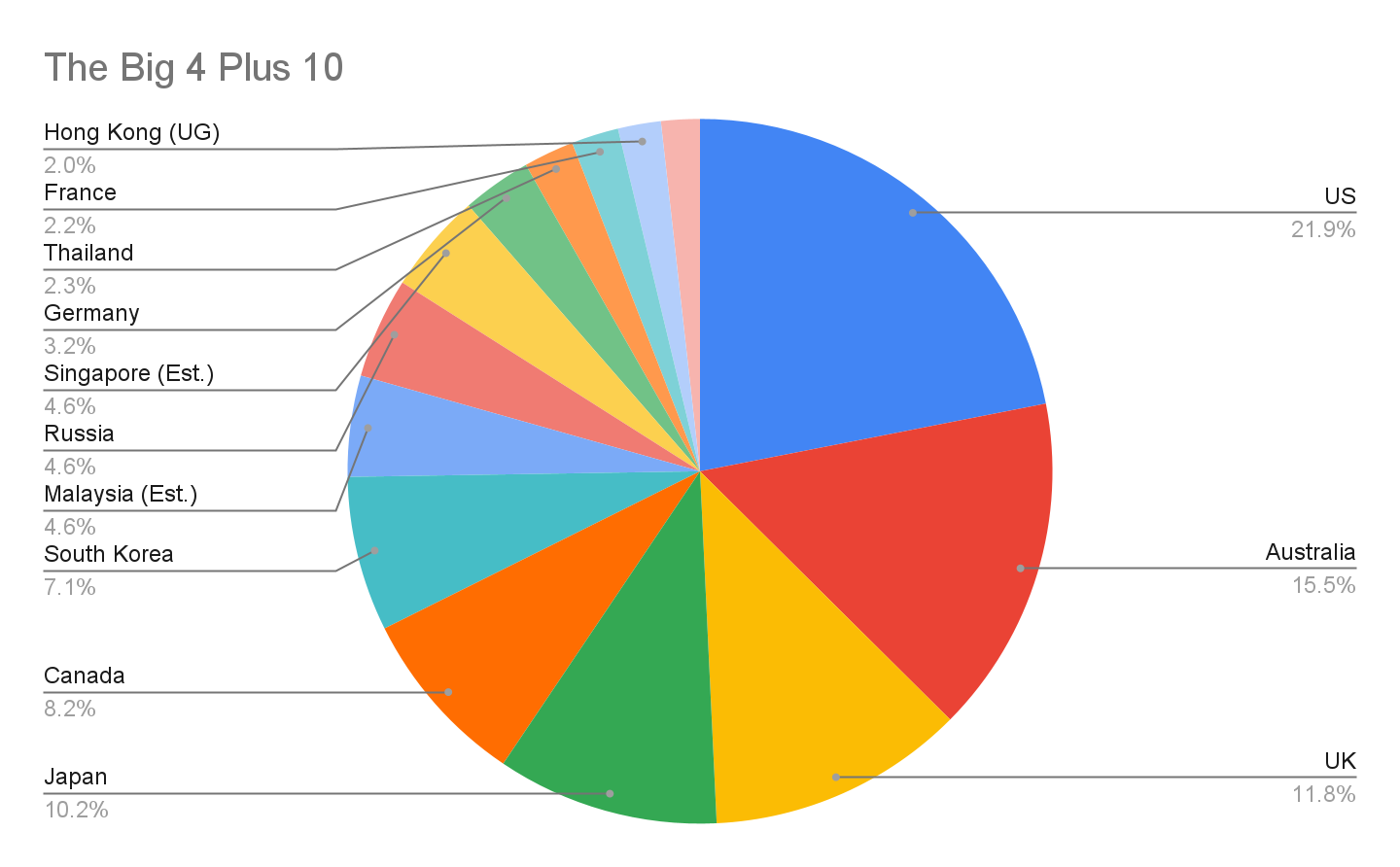

Total Chinese outbound enrollment for the most recent reporting year reached 1,213,053 students — a 6.15% increase from the prior year.

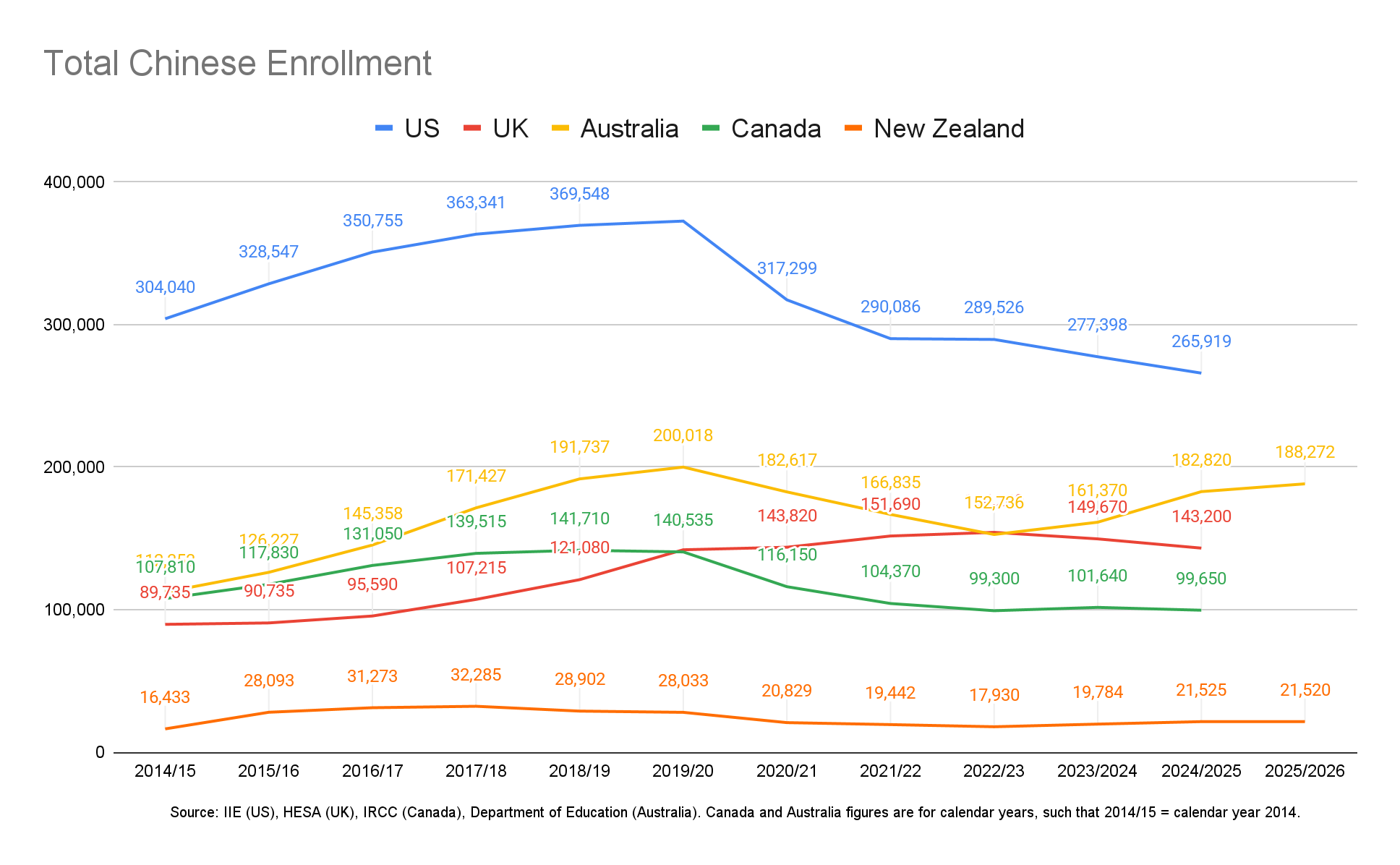

The "Big Four" anglophone destinations (US, UK, Australia, Canada) collectively enrolled 697,041 Chinese students, accounting for 57.4% of the total. The US and UK were both down approximately 4%, while Australia grew 3% and Canada declined 2%.

Meanwhile, Asian study destinations grew 26.2% collectively. Japan surpassed Canada in Chinese enrollment. South Korea is up 42%. Singapore and Thailand both grew roughly 50%. These numbers have generated some concern in international recruitment circles — but context matters.

Asian destinations are largely attracting families making a consumption decision: regional proximity, lower cost, peer networks close to home. Big Four destinations — particularly the US — attract families making an investment decision: a degree that changes career trajectories, opens PhD pathways, and commands a salary premium in China's most competitive job market. These are not competing for the same students.

One note of caution: Japan–China relations in 2026 will likely soften those numbers. Asian enrollment growth is not meaningfully displacing US recruitment.

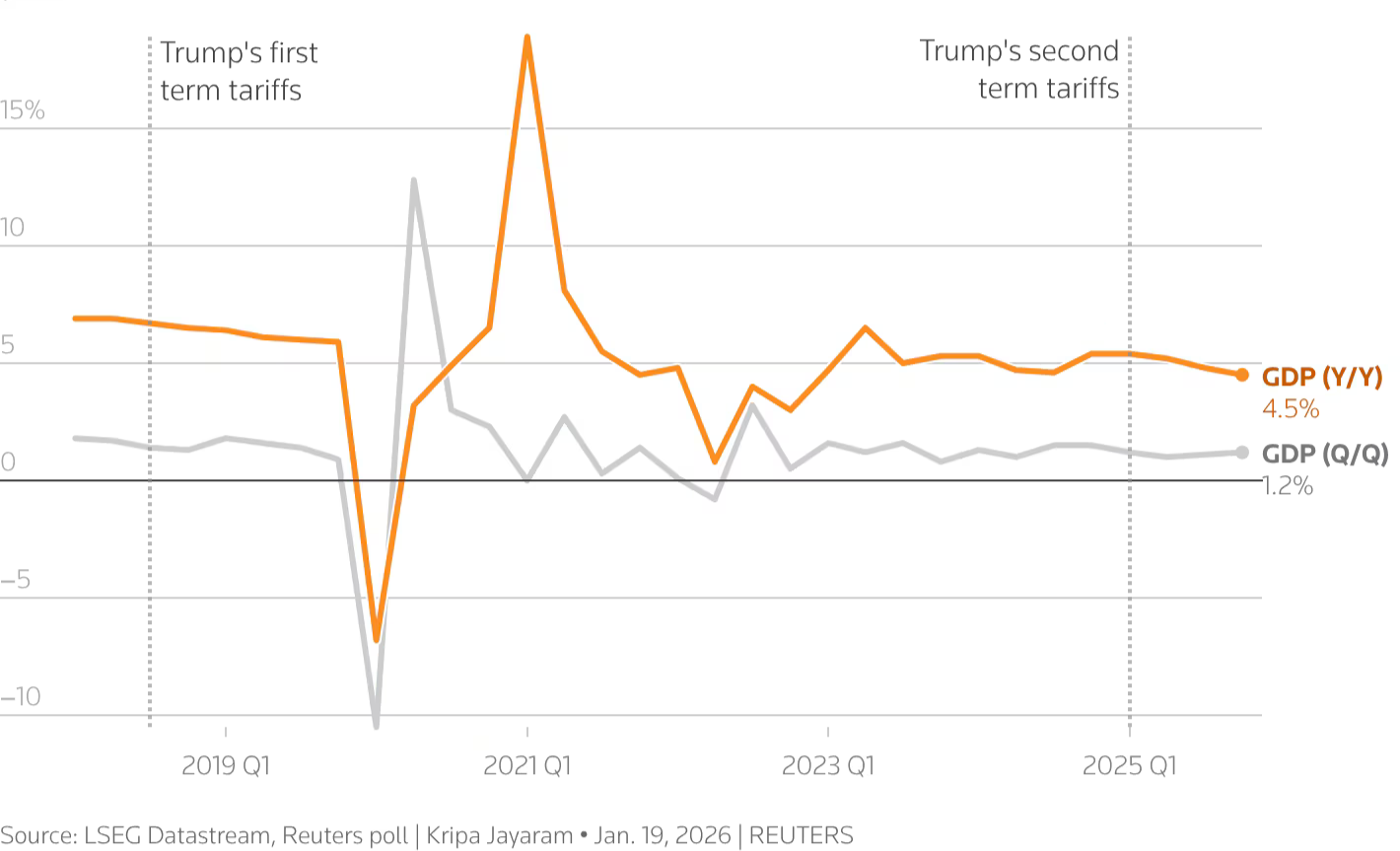

The Economic Backdrop

China's macro picture in 2026 is meaningfully stronger than it was in 2025.

GDP grew 5.0% in 2025 (official NBS figure; IMF projects 4.8% for 2026), with total economic output exceeding RMB 140 trillion for the first time. The Chinese yuan strengthened below 7:1 USD near the end of 2025 — its best level since 2023 — directly improving the affordability of overseas tuition for Chinese families. China posted a record trade surplus of approximately $1.2 trillion in 2025.

The tariff story, while dramatic, has been more contained than early headlines suggested. Reciprocal tariffs peaked at ~145% in April 2025, were cut to 10% in the May 12 truce, and extended through November 2026. Yale economists estimated the GDP impact on China at approximately 0.2%. China is substantially less reliant on US exports than it was in 2017.

The diplomatic calendar also looks constructive: a Trump–Beijing summit is reported for May/June 2026, with a reciprocal Xi visit under discussion. Summit diplomacy reliably reduces rhetorical heat — already visible in the approval of Nvidia H200 chip sales and a softer official tone since the trade deal was signed.

For universities maintaining China recruitment strategies: the fundamentals support the investment.

The New ROI of Overseas Study

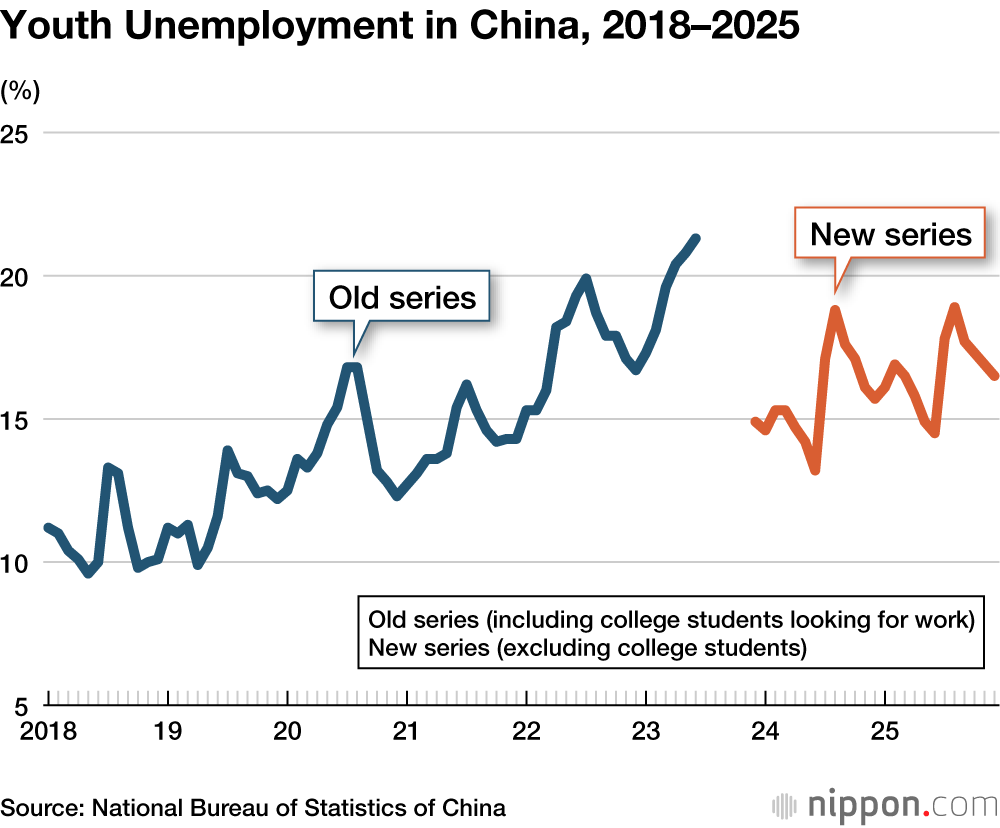

China's domestic job market is under significant pressure. Youth unemployment stood at 16.1% as of February 2026. A record 12.22 million graduates entered the labor market in 2025 — up 430,000 from 2024. More than 20% of food delivery platform drivers now hold college degrees.

This structural mismatch is reshaping what Chinese families look for in an overseas degree. It's no longer enough to simply hold a foreign credential. Families are increasingly focused on concrete employment outcomes — and this is creating meaningful opportunity for institutions that can speak directly to that ROI.

Two trends are particularly significant:

The Chuhai Effect. Intense domestic competition is pushing Chinese companies overseas at scale: BYD, ByteDance, DJI, SHEIN, Pop Mart, MiHoYo — all expanding international operations to escape saturated home markets. This reshapes the value proposition of a US degree entirely. It's no longer only about impressing a multinational recruiter. Chinese companies' global operations actively need staff with international experience, language fluency, and cross-cultural range. US work experience is now a selling point toward Chinese company global roles — not only US ones.

Overseas Returnees Are In Demand. An analysis of job ads from 36 Chinese universities found that 64% emphasized requirements related to an "overseas background." 80.85% of corporate HR professionals view international study experience as an advantage for candidates. Returnee talent inflows grew 12% in 2025 to an eight-year high.

The universities best positioned in this environment are those that can clearly articulate placement outcomes, highlight internship pathways, and connect their degree programs to growth industries: AI, green technology, finance, and advanced manufacturing.

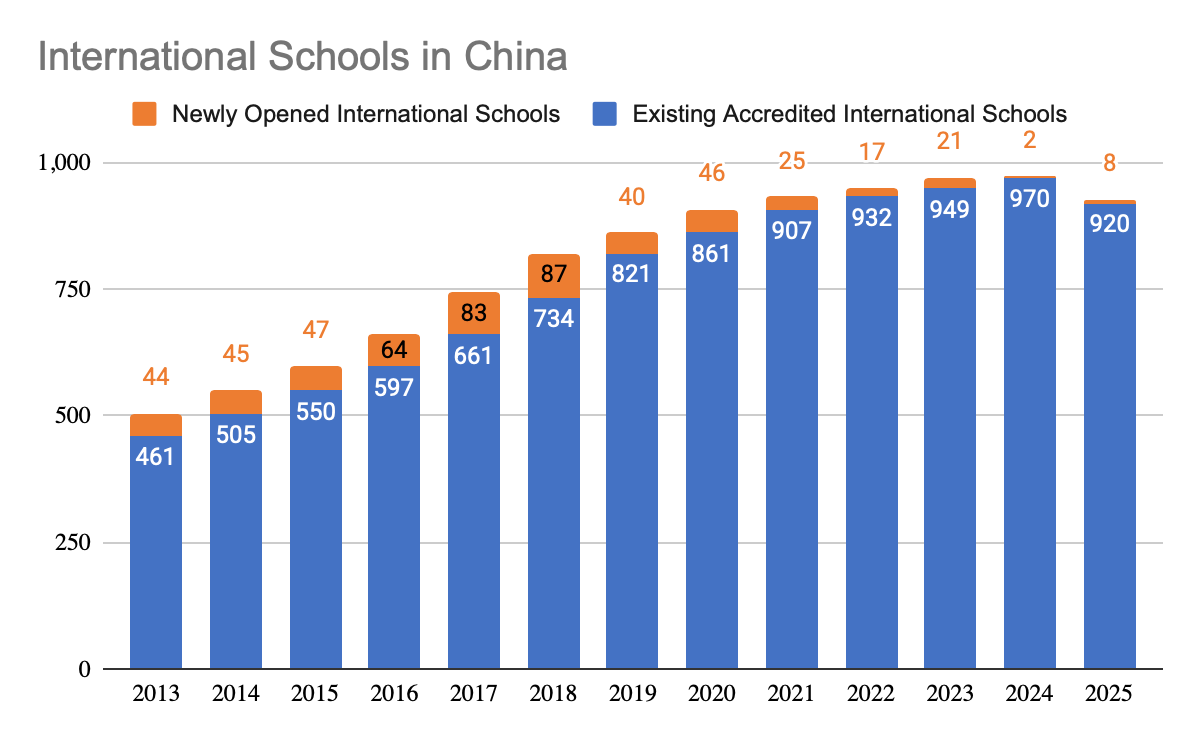

International Schools: The Early Indicator

China's international school sector remains an important leading indicator for undergraduate enrollment pipelines. As of 2025, 468,000 students were enrolled in international schools in China, paying average tuition of 129,000 RMB (flat from 2023). 70% of schools enroll fewer than 500 students.

Growth areas for international schools are shifting toward Tier 2 and 3 cities, which are more insulated from demographic pressures concentrated in major urban centers. In Southeast Asia, international school growth has been explosive: Thailand has nearly tripled its international school count in five years; Malaysia is up 11%.

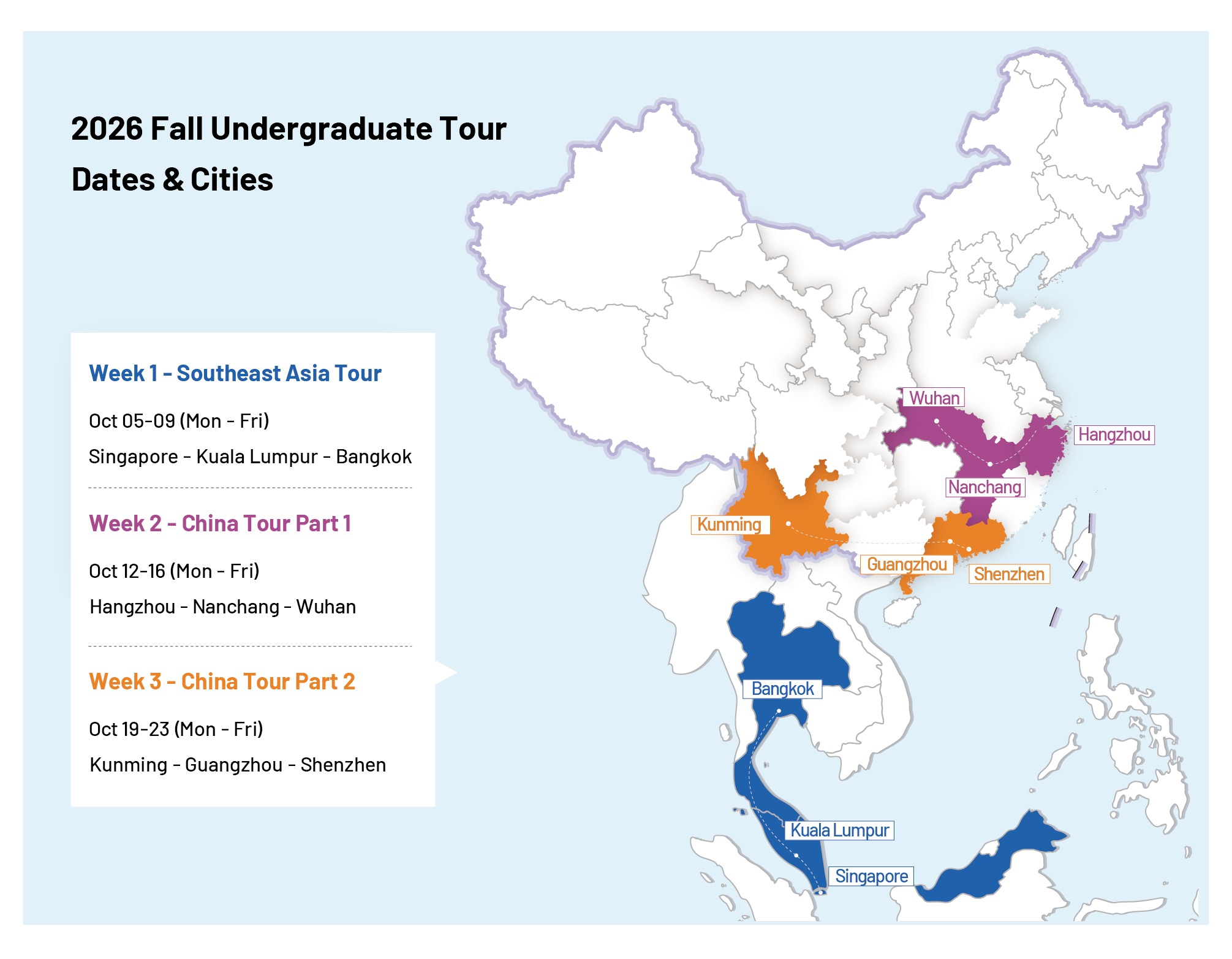

This is precisely why Sunrise has expanded its recruitment tours to include Southeast Asia this year. Our new Asia Undergraduate Recruitment Tour (October 5–9, 2026) takes university representatives to Singapore, Kuala Lumpur, and Bangkok — cities where international school enrollment is surging and where students are actively exploring US undergraduate options. It runs back-to-back with our China tours, giving institutions the option to cover both markets in a single trip.

The Agent Landscape

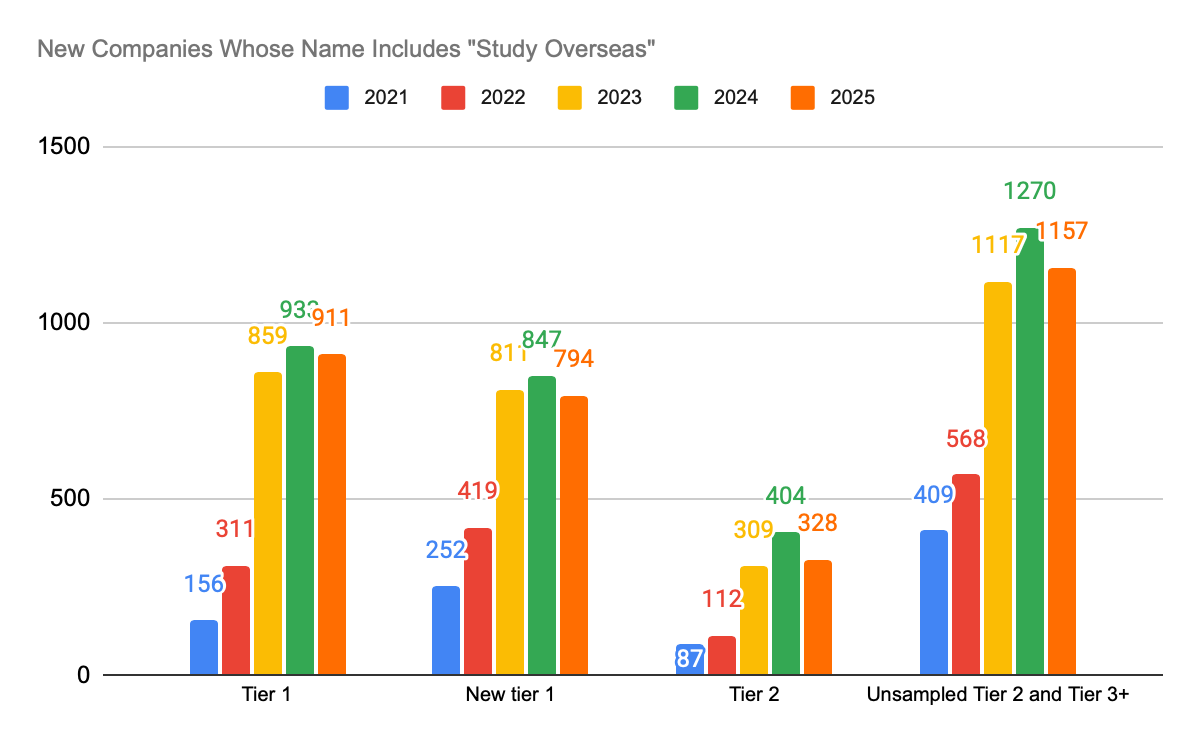

The study-abroad agency market in China is booming — and fragmenting simultaneously.

2025 saw 3,190 new companies registered with "study overseas" in their name, representing a 252% increase since 2021. New Oriental's study abroad division reported a 4.1% increase in net revenues, exceeding $439 million — a signal of sustained, growing demand.

Fragmentation creates both opportunity and complexity for universities. More agencies mean more coverage in more markets and cities. But it also means less familiarity with commission-based models and greater variability in service quality.

Technology is reshaping this landscape further. Direct admissions platforms are gaining traction. AI tools are blurring the line between traditional agents and application platforms. For now, traditional agents remain the most trusted resource for Chinese students and families — but institutions should be monitoring how this shifts over the next 18–24 months.

What This Means for 2026 Recruitment

For university enrollment teams, the key takeaways from this data are straightforward:

Don't conflate visa disruption with demand destruction. The 2025 visa drop was real — but Chinese student demand, as measured by application rates, agency growth, and family investment behavior, held firm. Institutions that reduced China engagement in 2025 may find themselves behind in 2026–27 pipelines.

Lead with ROI. Chinese families are more outcome-focused than ever. Programs that can connect overseas study to specific employment pathways — particularly in AI, green tech, finance, and with Chinese companies' international operations — have a compelling story to tell.

Invest in Tier 2 and 3 cities. Recruitment activity in Beijing, Shanghai, and Guangzhou is competitive and crowded. The next generation of Chinese students — and the agents serving them — is increasingly distributed across the country.

Stay engaged through the uncertainty. Summit diplomacy, a stronger RMB, and resilient GDP growth all point toward a more favorable environment in 2026–27. The institutions with existing relationships in China are the ones who will capture that rebound.

Sunrise International Education is a Beijing-based full-service media production and education company specializing in Chinese student recruitment and marketing. We work with 517+ member schools across content marketing, digital advertising, live events, and thought leadership.

Ready to meet students where the growth is? Our 2026 Fall Recruitment Tours run October 5–23, combining a brand-new Southeast Asia leg (Singapore, Kuala Lumpur, Bangkok) with two weeks of proven China coverage in Tier 2 and 3 cities. Early Bird pricing is available through June 1.